Getting PR in Singapore is not just about securing long-term residency; it also comes with financial benefits, including tax reliefs. As a Singapore PR, you enjoy greater stability, family security, and access to tax benefits that can significantly improve your financial health. In this guide, we’ll show you how Singapore PRs can maximise their tax reliefs every year through strategies like boosting CPF contributions, leveraging the Supplementary Retirement Scheme, and exploring other relief options. For those still planning to apply, check out Majestic Immigration to get expert guidance on your Singapore PR application.

Key Takeaways

- Becoming a Singapore PR brings more than just the advantage of residency. It also opens the door to substantial tax benefits that can greatly improve financial stability. The Inland Revenue Authority of Singapore (IRAS) has built a progressive tax system that, while ensuring fairness, also provides multiple reliefs to reduce taxable income. PRs are treated on par with Singapore Citizens, giving them access to reliefs that not only ease their yearly tax burden but also encourage responsible financial planning for retirement, family care, education, and even philanthropy.

- One of the biggest financial advantages for PRs lies in CPF contributions. Mandatory contributions are automatically deductible, and voluntary top-ups further reduce taxable income while growing long-term retirement funds at attractive interest rates. In addition to CPF, the Supplementary Retirement Scheme (SRS) provides another opportunity to reduce income taxes, offering PRs the flexibility to invest in a range of financial instruments, including stocks, ETFs, and insurance products. Taken together, CPF and SRS form a strong dual strategy. CPF provides guaranteed growth and retirement security, while SRS allows for investment-driven growth.

- Tax reliefs make the Singapore PR status more rewarding than just permanent residency. They reflect a system designed to promote financial stability, lifelong learning, and family support. For those still in the process of applying, these benefits serve as a crucial reminder that obtaining PR status is also an investment in long-term financial growth. With the right strategies, such as maximising CPF and SRS contributions, leveraging family-related reliefs, and incorporating donations, PRs can substantially reduce their tax liability every year while building a secure future in Singapore.

Overview of Tax Reliefs for Singapore PRs

Becoming a Singapore Permanent Resident (PR) offers more than just stability and long-term residency. One of the key financial advantages is access to a wide range of tax reliefs provided under the Inland Revenue Authority of Singapore (IRAS) framework. These reliefs are designed to reduce taxable income, helping individuals save more while building a secure future in Singapore.

How the IRAS Tax Framework Works

- Singapore follows a progressive tax system, meaning the higher your income, the higher the tax rate you pay.

- However, IRAS provides various personal tax reliefs, rebates, and deductions to lower your taxable income.

- These reliefs apply to both citizens and PRs, ensuring that Permanent Residents enjoy significant financial benefits while contributing to Singapore’s economy.

Key Benefits for PRs

Singapore PRs can tap into multiple reliefs that ease their financial burden:

- CPF Reliefs: Mandatory CPF contributions are tax-deductible, allowing PRs to save for retirement while lowering taxable income.

- Parent/Spouse Reliefs: Tax reductions for supporting immediate family members.

- Course Fee Relief: Deductions for skills upgrading and continuous learning.

- Life Insurance Relief: Applicable if CPF contributions are below the limit.

- Working Mother’s Child Relief (WMCR): For PR mothers balancing work and childcare.

These reliefs not only help PRs save on annual taxes but also promote long-term financial planning, education, and family support. Enjoying these tax advantages is one of the many reasons why applying for PR status is a smart move. If you are exploring your options, learn more about the process here: Apply PR SG with Majestic Immigration.

Types of Tax Reliefs Available to PRs

Singapore PRs who qualify as tax residents can benefit from a wide range of tax reliefs offered by IRAS. These reliefs lower taxable income, support retirement savings, encourage lifelong learning, and ease family-related expenses. Below is a summary of the main reliefs available:

| Type of Relief | Who Qualifies | Amount / Cap | Key Notes for PRs |

| CPF Contributions Relief | All PR employees making mandatory CPF contributions | Based on employee CPF contributions (20% of wages up to CPF wage ceiling) | Relief is automatic; CPF top-ups may qualify for additional relief under the Retirement Sum Topping-Up (RSTU) Scheme. |

| Earned Income Relief | All taxpayers earning income (employment, trade, profession) | Below 55: S$1,000 | Granted automatically; no claim needed. |

| Parent Relief / Handicapped Parent Relief | Taxpayers supporting parents or grandparents | Living with taxpayer: S$9,000 | Dependants must meet IRAS income/residency conditions. |

| Spouse Relief / Handicapped Spouse Relief | Married taxpayers supporting spouse | Up to S$2,000 (handicapped spouse: S$5,500) | A dependent spouse’s annual income must not exceed S$4,000, unless handicapped. |

| Qualifying Child Relief (QCR) / Handicapped Child Relief (HCR) | Parents supporting dependent children | QCR: S$4,000 per child | Children must be below 16, studying full-time, or disabled. Some benefits apply only if the child is a Singapore Citizen. |

| Course Fees Relief | Individuals paying for work-related or self-improvement courses | Up to S$5,500 per year | Courses must be relevant to current job or trade. Employer-sponsored or SkillsFuture-funded fees cannot be claimed. |

Singapore PRs have access to a wide range of tax reliefs that make living and working here more financially rewarding. From CPF contributions relief to family-related reliefs and course fees relief, these schemes are designed to support retirement planning, encourage family care, and promote upskilling.

Strategies to Maximise Tax Reliefs Every Year

While Singapore PRs benefit automatically from some reliefs (like CPF contributions and earned income relief), active planning can help you claim additional savings and reduce your taxable income. Below are strategies to make the most of available reliefs each year:

1. Use Your CPF Contributions

For Singapore PRs, maximising Central Provident Fund (CPF) contributions is one of the most effective ways to reduce taxable income while building long-term financial security. Beyond being a mandatory scheme, CPF offers multiple opportunities for tax savings through voluntary contributions and top-ups. So why do CPF contributions matter?

- Dual Benefits: Boost your retirement funds while lowering taxable income.

- Attractive Interest Rates: CPF Special and Retirement Accounts earn 4% per annum, with an additional 1% interest on the first S$30,000 for members aged 55 and above.

- Long-Term Security: CPF helps PRs accumulate savings for retirement, healthcare, and housing needs.

For PRs applying through schemes like PR application SG, strong financial planning and CPF top-ups demonstrate commitment to long-term settlement in Singapore.

CPF Top-Up Relief

CPF Top-Up Relief allows PRs to claim substantial tax deductions when making cash top-ups to their:

- Special Account (SA) – for members below 55

- Retirement Account (RA) – for members 55 and above

- Medisave Account (MA) – for healthcare expenses

Voluntary Contributions to CPF

Beyond mandatory contributions, PRs can make voluntary contributions (VCs) to boost CPF savings across accounts (Ordinary, Special, and Medisave). Let’s discuss the key advantages of voluntary contributions.

- Grow your retirement fund faster with attractive CPF interest rates.

- Reduce your taxable income through additional reliefs.

- For members 55 and above, extra interest makes voluntary contributions even more rewarding.

Pro Tip: Plan CPF top-ups early in the year, rather than waiting until the end of the year. This ensures funds enjoy compounding interest for a longer period while also securing your tax relief for that year.

2. Leverage Supplementary Retirement Scheme (SRS) Contributions

For Singapore PRs, the Supplementary Retirement Scheme (SRS) is a powerful but often overlooked way to save more for retirement while reducing taxable income. Unlike CPF, which has fixed contribution rules and withdrawal conditions, the SRS offers greater flexibility in contributions and investments. This makes it an excellent complement to CPF savings, especially for PRs planning long-term financial security in Singapore. So why consider the SRS?

- Dual Benefit: Immediate tax savings + long-term retirement growth.

- Flexibility: Contributions are voluntary, and the amount can vary from year to year.

- Investment Options: Wide range of choices, including insurance, unit trusts, stocks, ETFs, and robo-advisors.

- Tax-Deferred Growth: Earnings from investments accumulate tax-free until withdrawal.

For PRs preparing for retirement or in the middle of their PR application SG journey, demonstrating consistent savings habits through CPF and SRS contributions highlights a long-term commitment to Singapore.

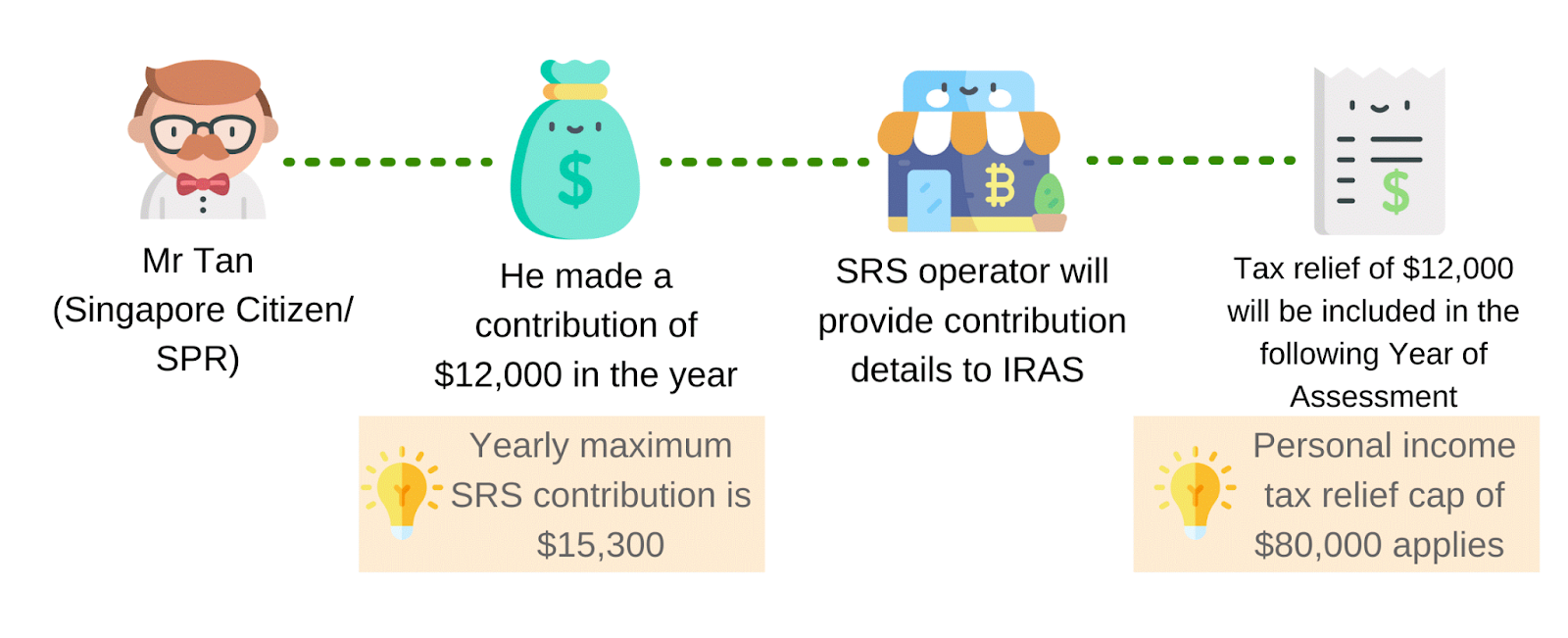

SRS Tax Relief

Contributing to SRS comes with automatic tax relief. Here’s how it works:

- Contributions reduce your chargeable income in the Year of Assessment following the contribution.

- No manual claim needed – the bank handling your SRS will report to IRAS.

- To qualify, you must be a Singapore tax resident.

- Contributions must be made by 31 December of the year to count.

Investing Your SRS Funds

Leaving SRS contributions idle means missing growth opportunities. Instead, consider investing them to maximise long-term returns:

- Unit Trusts and ETFs – diversify across markets and sectors.

- Insurance Products – Combine Protection with Long-Term Savings.

- Stocks and Bonds – direct exposure for higher (but riskier) returns.

- Robo-Advisors – automated platforms like StashAway offer diversified, low-cost portfolios tailored to your risk profile.

Investment gains stay in your SRS account and grow tax-deferred until withdrawal, giving your retirement savings a significant boost.

Pro Tip: Combine CPF Top-Ups and SRS contributions to maximise tax reliefs while diversifying your retirement savings. CPF gives guaranteed interest, while SRS provides growth potential through investments.

3. Claim Family-Related Reliefs

Singapore’s tax system recognises the financial responsibilities of supporting children and elderly parents by offering family-related tax reliefs. For Singapore PRs, these reliefs not only reduce taxable income but also provide meaningful financial support for dependants. By coordinating claims between spouses and understanding eligibility rules, you can maximise tax savings every year.

Coordinating Reliefs Between Spouses

- Reliefs such as Parent Relief and Qualifying Child Relief (QCR) can be shared between spouses.

- Couples should coordinate to ensure claims are optimised. e.g., assigning relief to the spouse with the higher income for greater tax savings.

- The total claim cannot exceed the relief cap, even if shared.

Parent Relief

This relief is available if you support your parents, grandparents, or parents-in-law. Eligibility conditions are:

- Dependants must be 55 years old and above, or physically/mentally disabled.

- Annual income of the dependant (including allowance and pensions) must not exceed S$8,000.

- You must have incurred costs in supporting the dependent (e.g., providing food, housing, or medical care).

Qualifying Child Relief (QCR)

This relief supports parents raising children.

- Eligibility Conditions: Child must be unmarried, and either:

-

-

- Below 16 years old, or

- Studying full-time, or

- Physically/mentally disabled.

- Annual income of the child must not exceed S$8,000.

-

-

-

- QCR: S$4,000 per child.

- Handicapped Child Relief (HCR): S$7,500 per child.

-

- Sharing Rules:

-

- Relief can be shared between parents (including divorced parents).

- Total relief per child is capped at the stated amount.

Pro Tip: Always assess whether to claim Parent Relief or allow your siblings to, since relief can only be claimed by one or shared. Similarly, couples should plan which spouse claims QCR/HCR for maximum tax savings.

4. Use Life Insurance Relief

Life insurance relief is another way Singapore PRs can reduce taxable income while ensuring financial protection for their families. By claiming relief on qualifying life insurance premiums, you can lower your annual tax burden by up to S$5,000. This makes it a practical option for those seeking both financial security and tax savings.

Eligible Life Insurance Plans

To qualify for Life Insurance Relief, the following conditions must be met:

- The policy must be in your own name or your spouse’s name.

- The insurer must have an office or branch in Singapore.

- CPF contributions in the preceding year must be below S$5,000 (including employee and voluntary contributions).

- Premiums paid must be for life insurance, not for hospitalisation, critical illness, or disability insurance policies.

Calculating Life Insurance Relief

The relief is capped at S$5,000 per year, and the amount you can claim depends on your CPF contributions and insurance policy value. The calculation formula is: Relief = Lower of:

- S$5,000 – CPF contributions (including employee and voluntary top-ups), OR

- 7% of the sum assured (insured value of the policy), OR

- Total premiums paid.

This ensures that you only claim the lowest of the three values, in line with IRAS rules.

Pro Tip: Life insurance relief is most relevant for older PRs or self-employed individuals, as salaried employees usually contribute more than S$5,000 annually to CPF and may therefore not qualify.

5. Take Advantage of Deductions for Donations

Donating to charitable causes in Singapore not only makes a positive impact on society but also comes with significant tax benefits. Contributions made to Institutions of a Public Character (IPCs) and approved charities qualify for a 250% tax deduction. This means that for every S$1 donated, you can deduct S$2.50 from your taxable income.

By incorporating charitable giving into your financial planning, you can support meaningful causes while strategically reducing your tax liability.

Eligible Donations

Donations must be made to IPCs or the Singapore Government (for community, educational, health, or other public purposes) to qualify. Eligible contributions include:

- Cash contributions

- Publicly traded shares

- Land or buildings

- Artefacts of national significance

- Sponsorships to IPCs (only if they do not provide commercial benefits such as advertising in return)

Impact of Donation Deductions

- 250% deduction rate: This is one of the most generous tax reliefs available in Singapore.

- Carry-forward option: Unused donations can be carried forward for up to 5 years, provided you remain a tax resident.

- High value compared to other reliefs: Unlike CPF or SRS contributions with caps, donation deductions can result in substantial tax savings if you make large charitable contributions.

Pro Tip: Always check the Charities/IPCs database on the Charity Portal to confirm whether the organisation you are donating to is approved for tax-deductible donations.

Common Mistakes PRs Make in Claiming Tax Reliefs

Even with multiple avenues for reducing taxable income, many Singapore PRs overlook key details when filing their taxes. These common mistakes can lead to missed savings or even complications with the Inland Revenue Authority of Singapore (IRAS). By understanding these pitfalls early, you can take full advantage of the reliefs available and avoid unnecessary stress.

1. Missing Claim Deadlines

Tax reliefs such as Course Fees Relief or Parent Relief must be submitted before IRAS’s stipulated deadlines each tax season. Missing these deadlines often results in lost opportunities for relief, as late claims are generally not accepted.

2. Incorrect Documentation

Certain reliefs require supporting documents, such as receipts for course fees, proof of donations, or medical certifications for dependent-related reliefs. Failure to maintain or submit the correct documents can result in the rejection of claims. Always keep your records organised and ready for submission.

3. Not Optimising Between Family Members

Reliefs like Qualifying Child Relief or Parent Relief can often be shared between spouses. Many PRs fail to optimise who should claim, resulting in lower overall tax savings. Coordinating between family members ensures that reliefs are maximised without exceeding limits.

Tax reliefs are one of the many financial benefits that make the Singapore PR status attractive.

When you apply for a PR application, it is not just about securing residency; it is also about enjoying the long-term perks, such as structured CPF contributions and multiple tax relief opportunities. Understanding how to claim and optimise these reliefs can significantly improve your financial position as a PR.

Pro Tip: Before filing, review IRAS’s e-Filing system to double-check your claims and consult a tax advisor if needed. Strategic planning ensures you do not miss out on the relief you are rightfully entitled to.

How Majestic Immigration Helps Singapore PRs Beyond the Application

Becoming a Singapore Permanent Resident (PR) unlocks the door to long-term stability, career opportunities, and financial benefits, including CPF contributions and tax reliefs. However, the journey does not end once you secure your PR status. At Majestic Immigration, we provide more than just application support. We guide you through the financial and lifestyle advantages of living as a PR in Singapore.

1. Expert Guidance for PR Application

Our consultants specialise in helping applicants successfully apply for PR by tailoring strategies to their profiles. From preparing the necessary documents to highlighting your strengths, we ensure that your application has the best chance of being approved.

2. Advising on Long-Term Financial Planning

Securing PR status means gaining access to CPF contributions, tax reliefs, and government schemes that can enhance your financial well-being. Majestic Immigration goes beyond paperwork by educating PRs on how to:

- Maximise CPF top-ups for retirement planning

- Leverage family-related reliefs for lower taxable income

- Explore property ownership benefits available only to PRs

3. Ongoing Support After Approval

We don’t stop once your PR is granted. Our team provides insights on integrating smoothly into Singapore’s financial and social systems, ensuring you fully enjoy the privileges of your new status.

Ready to enjoy the benefits of PR? Contact Majestic Immigration today and secure your future in Singapore.

Frequently Asked Questions

Can PR get tax relief?

Yes, Singapore Permanent Residents (PRs) can qualify for various tax reliefs, provided they meet specific conditions. One key criterion is spending at least 183 days in Singapore within the assessment year. PRs are generally taxed as residents, granting them access to the same reliefs as Singapore Citizens, including CPF reliefs, parent-child reliefs, and deductions for donations. However, the total tax relief any individual can claim in a year is capped at S$80,000.

What is the maximum amount of tax relief I can claim in a year?

The maximum tax relief cap is S$80,000 per Year of Assessment (YA). This includes all reliefs combined, such as CPF contributions, course fee relief, SRS contributions, and insurance premium relief. Even if you are eligible for more, the total relief cannot exceed this limit.

How can I qualify for CPF Top-Up Relief?

CPF Top-Up Relief is available when you make cash top-ups to your own or your family members’ Special Account (SA), Retirement Account (RA), or Medisave Account. To qualify, the recipient must have an annual income of S$8,000 or less in the previous year if they are not the taxpayer. This relief encourages retirement savings while reducing your chargeable income.

What are the benefits of contributing to the Supplementary Retirement Scheme (SRS)?

Contributions to the SRS offer immediate tax benefits by lowering your chargeable income, which reduces your tax payable. Additionally, SRS funds can be invested in various products, including bonds, shares, unit trusts, and fixed deposits. This means you enjoy both tax savings and potential investment growth, supporting a more secure retirement plan.

Can I claim tax relief for life insurance premiums?

Yes, tax relief for life insurance premiums is available, but it is subject to a cap of S$5,000 per year. This cap is combined with CPF relief, which means the amount of life insurance relief you can claim depends on how much CPF relief you already receive. Generally, if your CPF contributions are high, the life insurance tax relief amount may be reduced.